Economic & Market Perspective: July 2026

The first half of 2026 was shaped by several events that influenced both the economy and financial markets. Geopolitical conflict in the Middle East, uncertainty surrounding trade policy, higher oil prices, and changing expectations for Federal Reserve policy contributed to increased market volatility. Despite these headwinds, equity markets recovered during the second quarter as corporate earnings remained strong and investment in artificial intelligence continued to support business spending.

Earlier in the year, market leadership had begun to broaden beyond the largest technology companies. That trend temporarily reversed during the Iran conflict as higher oil prices renewed inflation concerns and bond markets shifted from pricing Federal Reserve rate cuts to the possibility of additional rate hikes. As tensions eased and interest rate expectations stabilized, broader market participation resumed.

Market Performance

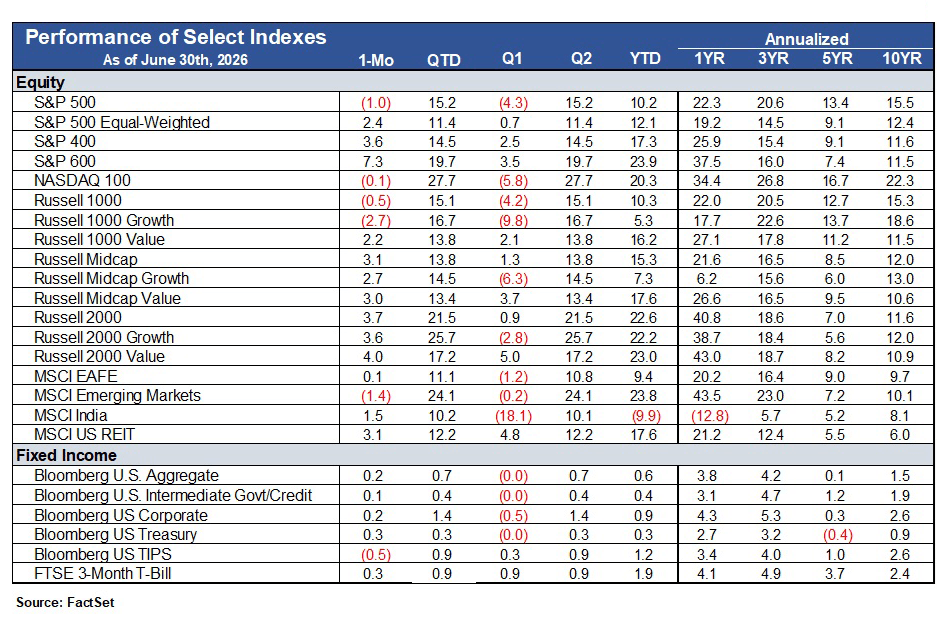

Equity markets recovered strongly in the second quarter to hit multiple all-time highs, after a pullback in the first quarter led to declines. The S&P 500® Index gained 15.2%, and the S&P 500 Equal Weight Index rose 11.4%.

Despite the shift to large-cap leadership during the quarter, the first half of 2026 still reflected broader participation across the market. Through June 30, the S&P 500 returned 10.2%, and the S&P 500 Equal Weight Index gained 12.1%. Small- and mid-cap stocks outperformed, with the Russell 2000® Index up 22.6% and the S&P 400 Index returning 17.3%%. International equities posted solid gains, with the MSCI EAFE Index rising 9.4%.

Fixed income returns were positive, but modest, as interest rates remained elevated. The Bloomberg U.S. Aggregate Bond Index returned 0.6% during the first half of 2026, while Intermediate Government/Credit bonds gained 0.4%. TIPS and 3-Month Treasury Bills returned 1.2% and 1.9%, respectively.

Overall, market gains in the first half of the year became less dependent on a small number of technology companies and broadened across more sectors and industries.

Earnings Growth

Corporate earnings were an important driver of market returns during the first half of the year. Strong earnings growth helped support the market, even as geopolitical events temporarily increased volatility. While price-to-earnings (P/E) multiples declined, earnings expectations continued to improve. Analysts currently expect S&P 500 earnings per share to grow approximately 24% in 2026 and 20% in 2027.

Technology companies remain the largest contributor to earnings growth, reflecting unprecedented spending by a handful of companies and sustained demand for artificial intelligence. Revenue growth has also become more broadly distributed across mid- and small-cap companies, providing support for earnings growth across a wider range of sectors. As a result, future market returns are likely to depend more on earnings growth than on higher P/E multiples.

The Economy

The U.S. economy remained resilient during the second quarter, although the first estimate of the second quarter Gross Domestic Product (GDP) will not be released until late July. Consumer spending supported economic activity, although spending patterns continued to differ across income groups. Higher-income households supported spending on travel, leisure and services, while lower-income consumers became more selective as higher borrowing costs and inflation, and rising gasoline prices earlier in the quarter, continued to pressure household budgets.

Business investment also remained healthy, supported in part by continued investment in artificial intelligence infrastructure, even as economic growth is expected to moderate from the strong pace seen over the past two years.

Trade is likely to weigh on the second-quarter GDP. Businesses accelerated imports amid continued uncertainty surrounding U.S. trade policy, which is likely to reduce the reported GDP growth rate, even though consumer spending and business investment remained resilient.

Labor Market, Inflation & the Federal Reserve

The labor market remained stable during the second quarter. June payrolls increased by 57,000, and prior months were revised lower. However, June followed three months of stronger job growth, with payroll increases averaging around 111,000 jobs per month. The unemployment rate declined to 4.2% from 4.3% and has gradually moved lower since late 2025.

Overall, the labor market appears to be cooling but not weakening. Payroll growth slowed to a more sustainable pace, wage growth remains consistent with a balanced labor market, and the unemployment rate remains historically low. As a result, inflation continues to be the primary focus for the Federal Reserve.

Inflation remained above the Federal Reserve's 2% target during the second quarter. While lower oil prices eased energy-related inflation pressures, shelter costs and labor-intensive service categories, including healthcare, transportation and restaurants, continued to keep underlying inflation elevated.

In June, Kevin Warsh took over as Chair of the Federal Reserve, which left its policy rate unchanged, maintaining the federal funds target range at 3.50% to 3.75%. Policymakers reiterated their commitment to returning inflation to the 2% target while acknowledging that the labor market remains relatively balanced. Future policy decisions are expected to remain data dependent, with inflation continuing to play the primary role in determining the timing of any policy changes.

Artificial Intelligence & Infrastructure Investments

Investment in AI remained strong during the quarter. Semiconductor companies continued to benefit, though spending increasingly shifted toward infrastructure needed to support AI, including data centers, networking equipment, power infrastructure and electrical equipment.

Meta announced that it would begin selling AI computing capacity to outside customers. The market initially focused on the competitive threat of Meta entering the AI cloud business, but the announcement also reinforced that the investment in AI infrastructure continues to expand beyond semiconductor companies.

Outlook

Looking ahead, we expect the U.S. economy to continue expanding at a more moderate pace. Inflation remains above the Federal Reserve’s target, and future policy decisions are likely to depend on continued progress toward lower inflation.

We believe that corporate earnings, rather than higher price-to-earnings multiples, will be the primary driver of future market returns. If earnings growth broadens across more sectors and industries, opportunities for investors may expand beyond the largest technology companies. While periods of volatility are inevitable, the underlying drivers of the market remain intact. Still, market leadership is unlikely to move in a straight line and will continue to respond to changes in the economic and geopolitical environment.

Jamie Zendel is EVP, Head of Quantitative and Asset Allocation Strategies, at Mutual of America Capital Management LLC.

Past performance is no guarantee of future results. The index returns discussed above are for illustrative purposes only and do not represent the performance of any investment or group of investments. Indexes are unmanaged and not subject to fees or expenses. The index returns above reflect the reinvestment of distributions. It is not possible to invest directly in an index.

The views expressed in this article are subject to change at any time based on market and other conditions and should not be construed as a recommendation. This article contains forward-looking statements, which speak only as of the date they were made and involve risks and uncertainties that could cause actual results to differ materially from those expressed herein. Readers are cautioned not to rely on our forward-looking statements.

The information has been provided as a general market commentary only and does not constitute legal, tax, accounting, other professional counsel or investment advice, is not predictive of future performance, and should not be construed as an offer to sell or a solicitation to buy any security or make an offer where otherwise unlawful. The information has been provided without taking into account the investment objective, financial situation or needs of any particular person. Mutual of America is not responsible for any subsequent investment advice given based on the information supplied.

Mutual of America Capital Management LLC is an indirect, wholly owned subsidiary of Mutual of America Life Insurance Company. Insurance products are issued by Mutual of America Life Insurance Company, 320 Park Avenue, New York, NY 10022-6839. Mutual of America Securities LLC, Member FINRA/SIPC distributes securities products. Mutual of America Retirement Services LLC provides administrative and recordkeeping services. Mutual of America Financial Group is the trade name for the companies of Mutual of America Life Insurance Company.